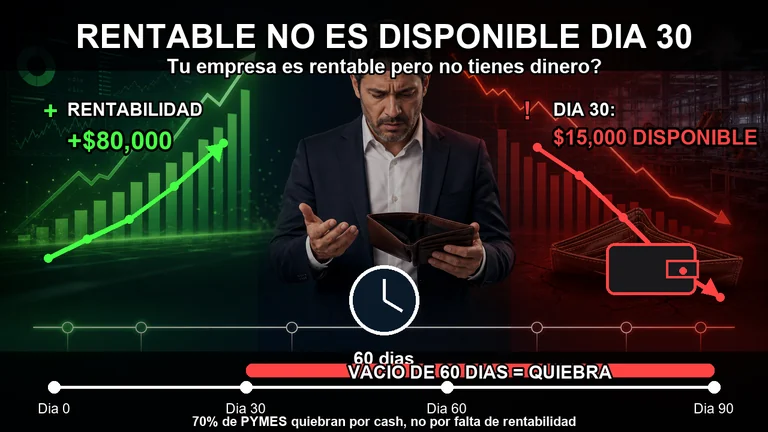

Many companies close the month with a financial statement that looks healthy. Sales are growing, operating margin appears positive, and the business seems profitable. Yet when day 30 arrives, reality becomes uncomfortable: suppliers must be paid, payroll is due, fixed commitments are immediate, and the bank account does not have enough cash.

This is one of the most dangerous paradoxes in business management: a company can be profitable on paper while facing serious liquidity risk.

Profitability measures whether the business is creating economic value. Cash measures whether that value is available to operate. Confusing these two concepts can lead to poor decisions, unnecessary debt, and constant financial pressure.

Profitability is not liquidity

An invoice is not money in the bank. A recorded sale is not necessarily available cash. And accounting profit does not pay suppliers.

Profitability is based on accrual logic: revenue and costs are recognized when they are generated. Liquidity answers a more direct question: how much real money does the company have available today to meet its obligations?

The invisible gap between selling and collecting

Consider a company with monthly sales of 200,000 dollars. On the income statement, the business may look healthy. But if it only collects 40% of those sales during the month, its real cash inflow is 80,000 dollars.

If the company must also cover 120,000 dollars in mandatory payments, the real cash result is not positive. It is a 40,000 dollar deficit.

Recorded sales: 200,000

Actual collections: 80,000

Mandatory payments: 120,000

Real cash balance: -40,000The company does not have a surplus. It has a financing need that must be covered through credit, reserves, delayed payments, or pressure on suppliers.

The risk of overproduction: when inventory consumes cash

Inventory can be an asset, but it can also become a liquidity trap. When a company produces faster than it sells or collects, it transforms cash into static product.

That product may appear as an asset on the balance sheet, but it cannot pay payroll, suppliers, or fixed expenses. It is cash trapped in inventory.

A practical inventory control rule

A useful liquidity principle is that inventory growth should not exceed real sales growth, except for a reasonable operational buffer.

Target inventory <= Expected sales + operating bufferIf inventory grows from 100,000 to 140,000 dollars without proportional demand, the company has not necessarily become stronger. It may have immobilized 40,000 dollars it needed to operate.

The anatomy of the cash gap

Cash flow does not depend only on how much the company sells. It depends on when it buys, when it produces, when it sells, and when it collects.

Day 0: materials are purchased

The company acquires raw materials or inputs. From this moment, there is already a financial commitment.

Day 30: the supplier is paid

Cash leaves the bank account even if the product has not yet been sold or collected.

Day 45: production is completed

The product is ready, but cash is still trapped in inventory.

Day 60: the sale is made

The company records the sale and may show revenue in its financial statements.

Day 90: the customer pays

Cash finally enters the business. The problem lies between day 30 and day 90: for those 60 days, the company is financing the operation with its own capital.

How to close the cash gap

The solution is not always to request more credit. In many cases, the first step is to redesign the financial timing of the operation by acting on three levers: collections, payments and inventory.

1. Improve collection speed

Collecting earlier can be more valuable than selling more. A sale that takes too long to become cash can put the entire operation under pressure.

- Identify customers with recurring payment delays.

- Offer selective early-payment discounts.

- Define clearer commercial terms.

- Follow up on accounts receivable weekly.

- Prioritize collection from strategic customers.

2. Negotiate better supplier terms

Not all suppliers have the same strategic weight. The objective is not to negotiate with everyone at once, but to identify the suppliers that matter most.

- Classify suppliers by spend, criticality and purchase frequency.

- Extend payment terms from 30 to 45 days where possible.

- Seek staged payment agreements.

- Consolidate purchases to improve conditions.

- Avoid reactive negotiations when cash is already under pressure.

3. Manage inventory with financial discipline

Inventory must be managed as a cash decision, not only as an operational decision. A company can significantly improve liquidity without selling more, simply by stopping unnecessary cash from being frozen in inventory.

The financial radar: a 90-day cash forecast

Managing a business by looking only at last month’s accounting close is like driving while looking in the rearview mirror. To protect liquidity, leadership must anticipate.

A 90-day cash forecast allows the company to project weekly inflows and outflows, identify future deficits, and act before pressure becomes crisis.

- Opening cash balance.

- Expected collections by customer.

- Committed supplier payments.

- Payroll and fixed expenses.

- Taxes and financial obligations.

- Planned purchases.

- Conservative, probable and optimistic scenarios.

From survival to scalability

A company that does not control cash flow operates in survival mode. It can sell, grow, and even report profit, but every month-end becomes a race against time.

A company that masters its cash cycle can invest with confidence, negotiate from a stronger position, grow without suffocating and protect operations when market conditions change.

Inventory + Collections + Payments = Operating liquidityConclusion: profit is not enough if cash does not arrive

Profitability matters, but it is not enough. Real financial strength appears when profitability becomes available cash.

If a company sells well but collects late; if it produces more than it needs; if it pays before recovering its money; or if it does not forecast cash in advance, it can face serious problems even with positive financial statements.

The strategic question is not only how much your company earns. The question is how much cash it has available, how many days of cash gap it must finance, and how long it can sustain operations without depending on debt or delayed payments.

At Roadvisors, we help companies turn financial and operational data into practical decisions that protect liquidity, improve profitability, and support controlled growth.

The final reflection is direct: if you reviewed your operation today, would you know exactly how many days of cash gap your company has before it runs out of financial oxygen?

Next step

Turn profitability into real liquidity.

Schedule a Roadvisors diagnostic to identify cash gaps, frozen inventory and operational decisions that affect your cash flow.